Selling your home while managing a health crisis and running your business requires strategic financial decisions that protect both your immediate wellbeing and your company’s future. When entrepreneur Maria Chen received her diagnosis, she had just three months to relocate closer to a specialized treatment center—her experience reveals crucial planning steps that prevented financial disaster.

Separate your personal home equity from business assets immediately by opening a dedicated health expense account before listing your property. This prevents the common mistake of co-mingling sale proceeds with business operating funds, which complicates tax planning and can jeopardize your company’s cash flow during your recovery period.

Calculate your true relocation budget by factoring in at least six months of reduced business involvement, not just moving costs. Most entrepreneurs underestimate how health challenges affect their earning capacity—financial advisor Robert Kim notes that clients who budget only for immediate medical expenses face cash shortages within 90 days.

Structure your home sale timeline around your business’s revenue cycle whenever possible. If you receive quarterly contracts or seasonal income, coordinate closing dates to coincide with cash influxes, providing financial cushioning for both medical expenses and business continuity.

Review your business entity structure with a CPA before closing, as home sale capital gains may interact unexpectedly with pass-through business income, potentially pushing you into higher tax brackets during an already expensive year.

Understanding the Financial Impact of a Health-Driven Home Sale

Why Entrepreneurs Face Unique Challenges

Canadian entrepreneurs face distinct obstacles when health issues force a home sale. Unlike traditional employees with predictable paychecks, your income likely fluctuates month-to-month, making it harder to demonstrate financial stability to buyers or qualify for bridge financing during the transition.

Many business owners have also leveraged home equity to fund their ventures, creating a complex financial web where personal and business assets intertwine. When you need to sell house due to ill health, untangling these connections becomes urgent yet complicated.

Consider Maria, a marketing consultant who discovered she needed immediate treatment requiring relocation. Her irregular quarterly payments and active client projects meant she couldn’t simply walk away. She needed a strategy that protected both her business reputation and financial future.

The pressure intensifies because you’re managing two critical transitions simultaneously: addressing your health needs while ensuring your business doesn’t collapse. Traditional financial advice rarely addresses this dual burden, leaving you to navigate loan obligations, client commitments, and medical decisions all at once.

The Real Costs Beyond the Sale Price

When calculating your home sale budget, look beyond the listing price to avoid financial surprises during an already stressful time. Selling costs typically consume 8-10% of your sale price, including real estate agent commissions (usually 5-6%), closing costs, potential repairs, and staging expenses.

Moving expenses add up quickly. Professional movers for a three-bedroom home average $2,000-$5,000 locally, or $4,000-$10,000 for long-distance moves. If you need temporary housing while searching for a more suitable property, budget for rental deposits, short-term lease premiums, and duplicate utility setups.

Medical transition costs deserve careful consideration. You might face gaps in healthcare coverage during relocation, overlapping insurance premiums, or out-of-network fees if changing providers mid-treatment. One entrepreneur shared how her unexpected three-month housing gap cost $6,000 in temporary rentals plus $1,200 in storage fees.

Business disruption represents another hidden expense. Relocating your operations might mean lost revenue during downtime, costs to update business addresses and licenses, or investing in remote infrastructure. Plan for at least 2-4 weeks of reduced productivity and factor this into your cash flow projections. Building a 15-20% contingency fund above your estimated costs provides essential breathing room when health matters demand your immediate attention.

Timing Your Sale: Balancing Health Needs and Financial Goals

Assessing Your Timeline Realistically

Your health timeline may not align perfectly with ideal market conditions, and that’s okay. The key is finding a realistic middle ground that protects both your wellbeing and your financial future.

Start by getting specific with your healthcare providers about timing. Do you need to relocate within 30 days, 90 days, or six months? This clarity becomes your anchor point for all financial decisions.

Consider Maria, a marketing consultant who needed specialized cardiac care three states away. Her doctor recommended relocation within 60 days, but local market conditions suggested waiting four months for better pricing. She chose a hybrid approach: listing immediately at a competitive price while maintaining her remote consulting contracts, which covered the difference between her ideal sale price and the realistic 60-day market value.

Similarly, James, a restaurant owner, faced an immediate health crisis requiring selling your house fast. Rather than waiting for spring’s higher prices, he accepted a fair winter offer and redirected saved energy toward his recovery and business transition planning.

Remember, the financial cost of delaying necessary health treatment often exceeds any potential gains from waiting for better market timing. Your goal isn’t maximum profit—it’s optimal outcome given your unique circumstances. Build buffer time into your timeline for unexpected complications, whether medical or transactional.

Tax Considerations You Can’t Afford to Miss

Selling your home during a health crisis comes with tax implications that can significantly impact your financial recovery. The good news? Several provisions exist specifically to help homeowners in your situation.

The primary residence exclusion remains your strongest ally. If you’ve lived in your home for at least two of the past five years, you can exclude up to $250,000 in capital gains as a single filer or $500,000 if married filing jointly. Even if you haven’t met the two-year requirement, you may qualify for a partial exclusion due to unforeseen health circumstances requiring a physician’s care.

Medical expense deductions deserve careful attention. According to tax expert Maria Chen, CPA, “Many entrepreneurs overlook that home sale proceeds used for qualified medical expenses exceeding 7.5% of adjusted gross income may be deductible.” This includes treatments, hospital stays, and even certain home modifications or assisted living costs.

Timing your sale strategically matters. If possible, coordinate the closing date to align with your tax year planning. Consider whether selling before or after year-end benefits your overall tax situation, especially if you’re closing your business simultaneously.

Don’t navigate these waters alone. Consult a tax professional familiar with both business ownership and medical expense deductions. They’ll identify state-specific considerations and ensure you’re maximizing every available benefit during this challenging transition.

Protecting Your Business While Managing the Sale

Separating Business and Personal Finances

When selling your home for health reasons, keeping your personal windfall separate from your business accounts is essential for both financial clarity and legal protection. Start by opening a dedicated personal savings account specifically for your home sale proceeds—this prevents the temptation to use these funds as an emergency business cash reserve and maintains clean accounting records.

Create a written plan documenting how much of the proceeds will cover immediate health expenses, living costs during recovery, and long-term personal savings. If your business requires capital during this transition, treat any transfer as a formal loan with documented terms and repayment schedules, just as you would with an external lender. This approach protects your personal safety net while maintaining proper business records.

Consider this real-world example: Maria, a marketing consultant, deposited her home sale proceeds into her business account “temporarily” to cover payroll during her treatment. Without proper documentation, she faced complicated tax implications and difficulty tracking personal versus business expenses. Working with her accountant, she restructured the transaction as a formal owner loan, establishing clear boundaries and incorporating it into her business continuity planning.

Consult both a tax professional and financial advisor to understand the implications of any fund transfers and ensure you’re maximizing tax advantages while protecting your personal financial recovery.

When Your Business Operates from Home

When your business operates from the same property you’re selling, you’ll need a thoughtful transition strategy that protects both your health and your professional reputation. Start planning your relocation at least 60-90 days before listing your home, giving you time to establish continuity for your clients.

Communication is essential. Inform key clients about your upcoming move early, emphasizing that your service quality won’t be affected. Sarah, a graphic designer who relocated due to chronic health issues, sent personalized emails to her top clients two months ahead, offering a small discount during the transition period. This transparency actually strengthened her relationships rather than damaging them.

Consider establishing your new business location before selling. If you’re downsizing or moving to a rental, set up a dedicated workspace immediately. This might mean using a coworking space temporarily or designating a professional area in your new home before your current property even lists.

Update your business address systematically across all platforms: website, Google Business Profile, social media, invoices, and bank accounts. Create a simple redirect message on your old business phone number to maintain professional continuity.

Remember, many successful entrepreneurs have navigated location changes while managing health challenges. Your clients value your expertise and service, not your physical address. With proper planning and clear communication, your business can thrive through this transition while you prioritize your wellbeing.

Making Smart Decisions with Your Sale Proceeds

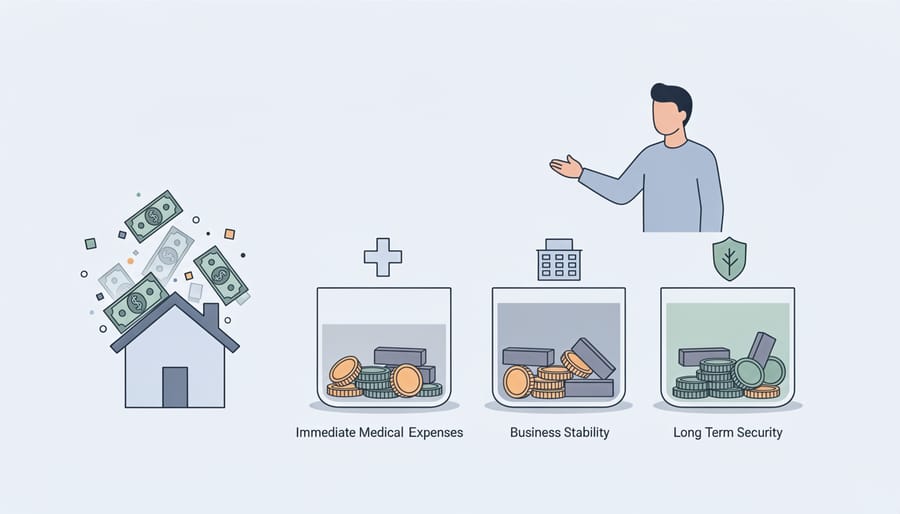

Creating a Three-Bucket Strategy

When selling your home for health reasons, strategic financial planning requires dividing your proceeds into three distinct buckets that address both immediate and future needs while protecting your business.

Start with Bucket One: Immediate Medical and Housing Needs (40-50% of proceeds). This covers urgent healthcare costs, medical equipment, home modifications, or temporary housing during treatment. Sarah, a marketing consultant who sold her home while managing cancer treatment, allocated 45% to cover six months of medical expenses and a rental deposit in a community closer to her treatment center. This gave her breathing room without depleting all resources.

Bucket Two: Business Stability Fund (25-35% of proceeds). This critical buffer maintains your business during reduced working capacity. It should cover 6-12 months of essential business expenses including payroll, rent, insurance, and key vendor contracts. Michael, a restaurant owner, set aside 30% to keep his staff employed and maintain supplier relationships while recovering from surgery, allowing his business to continue generating revenue even with limited involvement.

Bucket Three: Long-term Reserves (20-30% of proceeds). This bucket serves as your safety net for extended recovery or unexpected complications. Consider placing these funds in a high-yield savings account or conservative investment vehicle that remains accessible. This reserve also provides psychological comfort during a stressful time.

The exact percentages depend on your specific situation, but this three-bucket approach ensures you address immediate crises while safeguarding your entrepreneurial future.

Avoiding Common Financial Pitfalls

When sudden liquidity arrives from a home sale, entrepreneurs often stumble into predictable traps that can jeopardize both their financial security and health recovery. Understanding these pitfalls helps you protect your newfound resources during this vulnerable transition.

The most common mistake is immediately funneling sale proceeds back into your business. While your entrepreneurial instincts may push you to seize growth opportunities, remember that your health situation created this sale in the first place. Sarah, a restaurant owner who sold her home after a cancer diagnosis, initially planned to invest her entire $180,000 profit into expanding her business. Her financial advisor helped her recognize that without adequate personal reserves, a medical setback could force her to liquidate business assets at unfavorable terms.

Another critical error is maintaining an inadequate emergency fund. Entrepreneurs often underestimate their needs, forgetting that health issues can reduce income while increasing expenses. Financial experts recommend setting aside six to twelve months of living expenses, not the standard three to six months, because your recovery timeline may be unpredictable and business income can fluctuate.

Many entrepreneurs also neglect insurance planning during this transition. The stress of relocating and managing health concerns shouldn’t derail obtaining proper disability insurance, updated life insurance, or appropriate health coverage. These protections become essential when your earning capacity faces uncertainty. Consider consulting with an insurance specialist who understands entrepreneurial income structures to ensure your coverage matches your actual needs, not just your current premium budget.

Building Your Support Team

Essential Professionals for Your Situation

Assembling the right team of professionals can make the difference between a smooth transition and costly mistakes when selling your home while managing health challenges and running a business.

Start with a real estate agent who has experience with time-sensitive sales. Look for someone who understands your urgency but won’t push you toward underpricing. Ask potential agents how they’ve handled urgent sales before and request references from sellers in similar situations. The right agent will balance speed with market value.

A financial planner familiar with entrepreneurial finances is essential. Unlike traditional planners, they understand irregular income streams, business equity, and the connection between personal and business finances. They can help you integrate your home sale proceeds into broader strategic planning for both your health needs and business continuity.

Don’t overlook a tax professional who specializes in small business owners. Selling your home while owning a business can create complex tax implications, especially if you’ve used part of your property for business purposes. They’ll help you maximize deductions and minimize capital gains tax.

Finally, consider engaging your business advisor or accountant to ensure the sale doesn’t inadvertently affect your company’s financial position or creditworthiness. This coordinated approach protects both your personal recovery and your business interests.

Questions to Ask Before You Hire

Finding the right professionals during this challenging time requires asking targeted questions. When interviewing financial advisors, ask: “Have you worked with entrepreneurs selling assets due to health needs?” and “How will you help me minimize tax impact while maintaining business continuity?” Their responses will reveal their expertise level.

For real estate agents, inquire: “What’s your experience with health-motivated sales that need to close quickly?” and “How do you balance speed with maximizing value?” A seasoned agent will outline specific strategies for urgent sales.

When consulting healthcare financial planners, ask: “How do you coordinate between my business finances and medical expense planning?” This integration matters tremendously for entrepreneurs.

Don’t hesitate to request references from clients in similar situations. One entrepreneur shared that her advisor’s experience with business owners facing medical challenges helped her structure her sale to preserve retirement funds while covering immediate treatment costs. The right professional won’t just understand entrepreneurship—they’ll grasp the emotional weight of your health-driven timeline.

Planning for Your New Living Situation

Rent vs. Buy: What Makes Sense Now

When health challenges arise, the rent-versus-buy decision shifts from investment strategy to quality of life. Renting offers crucial flexibility if your health needs may change—whether that means relocating closer to specialized care, downsizing quickly, or avoiding maintenance responsibilities during treatment. You’ll preserve your capital from the sale for medical expenses and business continuity rather than tying it up in another property.

However, buying might make sense if you’ve found a home specifically designed for your health needs, such as single-level living or proximity to ongoing care providers. Consider this: Sarah, a tech entrepreneur, initially rented after her diagnosis, which gave her freedom to focus on treatment without worrying about selling again. After two years in remission, she purchased a modest condo near her clinic.

The key question is predictability. If your health timeline is uncertain, renting provides breathing room to make long-term decisions without pressure, while protecting the financial cushion you’ve just created from your home sale.

Budgeting for Accessibility and Health Features

When planning your next home, allocate funds specifically for health-related modifications. These investments directly support your wellbeing while protecting your business productivity.

Start by itemizing essential features. A consultant who needed a ground-floor bedroom allocated $8,000 for converting a dining room, including accessible bathroom modifications. An entrepreneur managing chronic fatigue budgeted $5,000 for improved ventilation systems and natural lighting upgrades that reduced daily symptoms.

Common accessibility costs include wheelchair ramps ($1,200-$3,000), walk-in showers ($3,500-$7,000), and wider doorways ($500-$1,000 per door). Climate control improvements for respiratory conditions typically range from $2,000-$6,000.

Consider setting aside 15-20% of your housing budget for these modifications. Many entrepreneurs underestimate these expenses, creating financial stress later. Research local grants and tax credits for accessibility improvements, which can offset 10-30% of costs in some regions. Request detailed quotes from contractors experienced in health-related renovations before finalizing your budget. This proactive approach ensures your new home genuinely supports both your health recovery and continued business success.

Selling your home for health reasons while managing a business is undeniably challenging, but you don’t have to navigate this transition alone. The strategies outlined here—from understanding your home’s equity and tax implications to protecting your business operations and planning for future housing needs—provide a solid foundation for making informed decisions during this difficult time.

Remember that Sandra, the e-commerce entrepreneur we discussed earlier, successfully maintained her business while relocating for treatment by creating a clear financial timeline and assembling the right support team. You can do the same. Start by prioritizing your immediate actions: consult with a financial advisor who understands entrepreneurial finances, connect with a real estate professional experienced in health-related sales, and review your business structure to ensure continuity.

This situation requires you to be both compassionate with yourself and strategic in your approach. Your health comes first, and with thoughtful planning, your financial stability and business can remain intact throughout this transition. Take it one step at a time, lean on professionals who can guide you, and trust that the effort you invest in planning now will create the breathing room you need to focus on what matters most—your recovery and well-being.